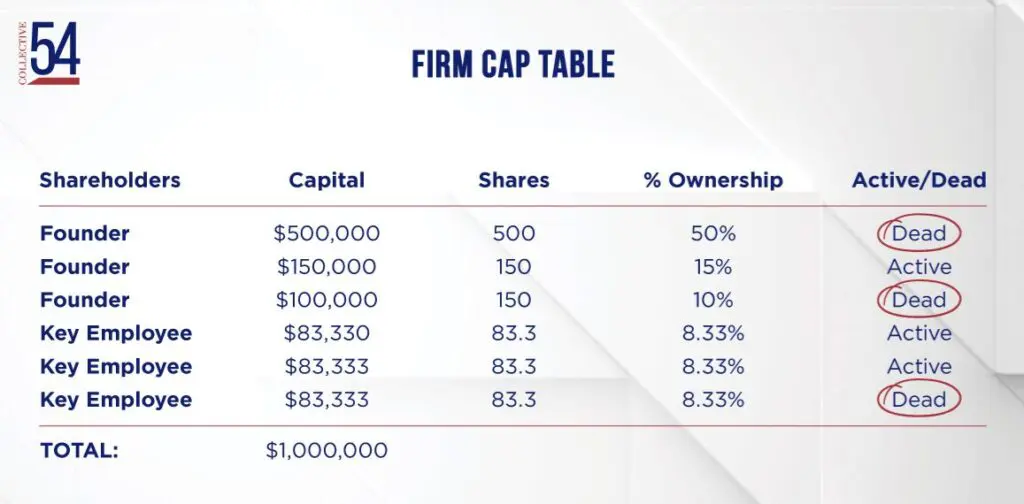

Do You Want to Be Rich or Be King?

In 2010, Clayton Christensen, renowned professor at Harvard Business School and author of The Innovator’s Dilemma introduced a concept that every founder must eventually confront: the choice between being Rich or being King.