The Hidden Cost Drivers of a Boutique Professional Service Firm

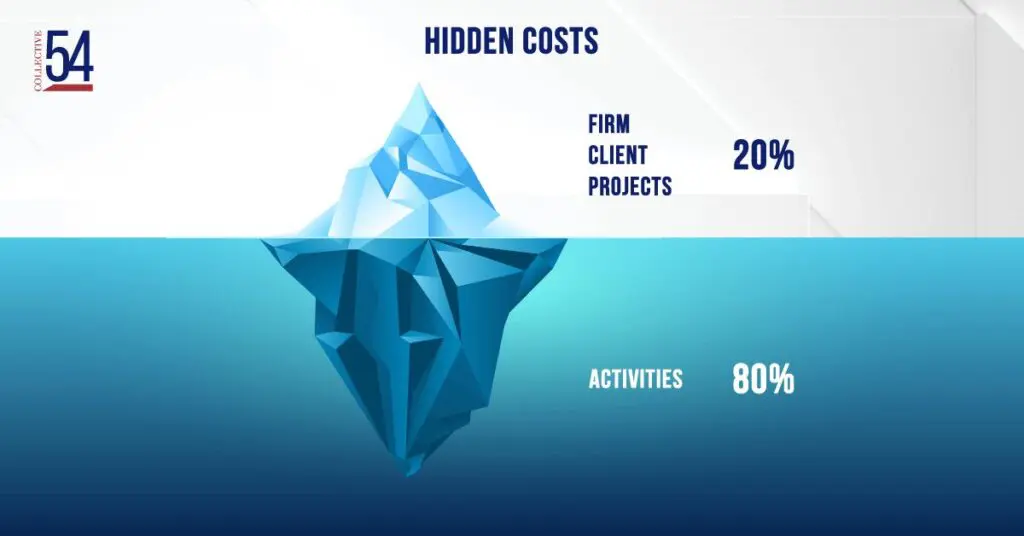

The real cost to run a boutique professional service firm is hidden from most founders because many founders use the […]

The real cost to run a boutique professional service firm is hidden from most founders because many founders use the […]