Why Founders Get Trapped in a Lifestyle Business

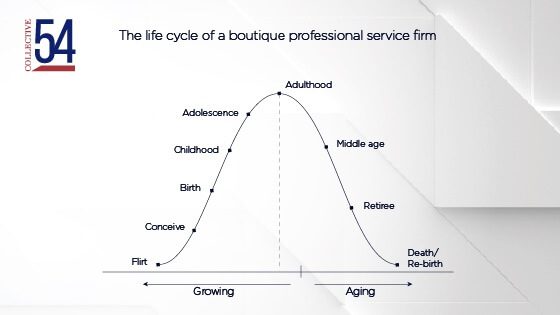

This article was originally published on CEOWORLD Magazine. In the boutique professional services industry, there are “young” 10-year-old firms and “old” […]

This article was originally published on CEOWORLD Magazine. In the boutique professional services industry, there are “young” 10-year-old firms and “old” […]

Someday you will sell your firm. Afterall, none of us can run our firms from the afterlife. When your time to exit comes, you will need to know what your firm is worth. The tool often used to calculate a purchase price is called a QOE, or the quality of earnings report. On this episode, QOE expert Elliott Holland, Founder & CEO at Guardian Due Diligence, will help founders understand what a QOE is, when it is needed, who creates one, how it gets used, and why founders need to get familiar with it.